The Longevity Lottery

Willard Scott can't keep up! It's no longer unique or surprising when we come across someone who is approaching age 100. We probably have someone in our own immediate family going strong at 85, 90 or even 95 years old. Whether because of good genes, healthy living, medical improvements or all of the above, living longer is a reality.

The blessing of a long life has many advantages but it also requires that we think about how to pay for that extended number of years. The axiom that people fear "running out of money" more than they fear death is truer today than ever before. The major risks to running out of money are market volatility, medical costs and spending too much. Of course, we have to accept some level of market risk if we want a decent return on our assets, we try to control our spending (but we also want to enjoy our success) and we do our best to live healthy — but to a great degree two out of three are not in our control.

In the investment world if you have a large gain in a concentrated position you can use a "collar" to "hedge" your bet. Simply put you "spend" some of the upside to "protect" the gain from risk of extreme loss. It is a form of insurance.

It is no different with the risk of longevity. We can spend a small percentage of our retirement assets (either out of the annual growth or capital) to protect us from running out of money in old age. Today's modern life insurance products offer living benefits that make our products more relevant and meaningful than ever before. Life insurance for the living!

We have all heard lots about Chronic Care/LTC riders combined with a life insurance policy. These riders are offered on dozens of products and all product types. And they do an amazing job protecting against the "getting sick" risk and helping to preserve our retirement assets for a long life.

But what if we could also guarantee annual cash flow from a life insurance policy? What if we could combine the assurances of death benefit protection with the security of annuity-type income? Now, there is such a product: AIG's Lifestyle Income Solution.

The Lifestyle Income Solution rider allows the policyowner to receive up to 10% of the death benefit in cash annually for 10 years beginning at age 85. This is not the policy cash value, which is subject to performance risk, this is the death benefitamount. The rider requires that you fund the policy at a certain level and the policy and rider must be in effect for at least 15 years prior to exercising the rider.

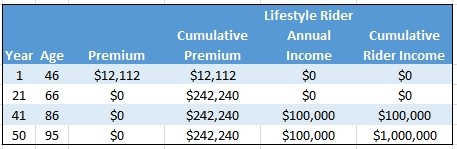

Let's look at an example.

Male 45, 20 pay, face amount $1,000,000, annual premium $12,112 for 20 years, Lifestyle income distributed for 10 years starting at age 86

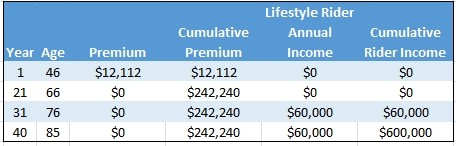

That's a return of over 4 times the premiums paid! But what if your client needs the money earlier than age 85? No problem. The policyowner can turn on the benefit, at a discount, any time after the policy and rider have been in effect for 15 years. In the example below the policyowner needs the money at age 76. As you can see they still get nearly 2.5 times the premiums paid in benefits over 10 years.

So what's the downside? Well, once the policyowner has received back their basis (premiums paid) any future distributions are taxable as ordinary income (just like a distribution from a qualified retirement plan). Still, remember the old adage: "Even taxable money is better than none at all."

The Lifestyle Solution Income rider is one product that offers:

- Death Benefit protection

- Chronic illness protection

- Retirement income protection

- Terminal illness access

- Return of premium (money back) protection

This solution is great for Executives (golden handcuffs), Professionals, Business Owners or anyone who wants to "hedge" their bet on winning the longevity lottery.

Give us a call at Windsor for customized case design and illustrations using the AIG Secure Lifetime approach. Or visit www.retirestronger.com for marketing material you can use with clients and advisors.

This information is for Agent and Broker Use Only and is Not for Use with the General Public. These materials are for general informational purposes only and should not be construed as legal or tax advice. Anyone considering the implementation of the concepts, strategies or ideas discussed in these materials should consult their own tax and legal advisors. Circular 230 Notice: This material was not intended or written to be used, and cannot be used, to avoid penalties under the Internal Revenue Code.

The life insurance illustrations associated with this blog assume the nonguaranteed values shown continue in all years. This is not likely, and actual results will be more or less favorable. Values shown are not valid unless accompanied by a basic illustration from the issuing life insurance company.

Comments