Policy Loan Rescue Strategies and Section 1035

The popularity of Index Universal Life products has stirred up the creative talents of many professional financial advisors, and nowhere has that creativity been more apparent than in the area of policy loan rescues. No question this is a significant opportunity to bring value to clients and generate a new sale, but it requires a high degree of expertise to navigate successfully. This article will review rescue strategies so that you have a better idea of what works and what doesn't. In addition, the Windsor case design team is fully conversant on the options and approaches that can generate a winning solution for you and your client. We welcome the opportunity to assist.

The "double whammy" of policy loan interest and malnourished policy values in a low interest environment can result in required increases in outlay that advisors and their clients did not anticipate. Policy loan rescue programs can ease or eliminate the burden of policy loans and loan interest, stopping the erosive effects of loan interest on policy values and establishing a new foundation that better supports and maintains the death benefit. To get started, let's do a quick review of the provisions of Internal Revenue Code Section 1035.

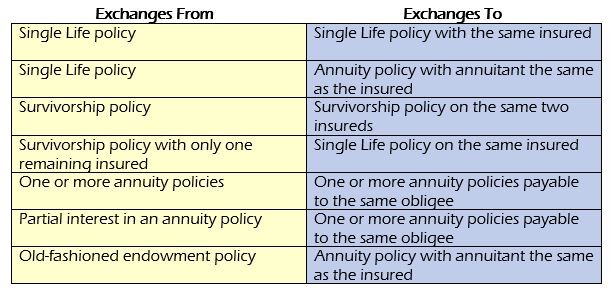

IRC §1035 allows the gain in a life insurance contract or annuity to be transferred to another contract without adverse tax consequences as a result of the exchange. But like all things governmental, there are a few rules. The table below will give you a quick idea of what's allowed – anything not in the table probably is not a tax-free exchange under §1035.

The guiding principles to remember in all this? From the government's point of view — (1) tax is better than no tax; and (2) the earlier tax comes out of a policy the happier the US Treasury. So moving from a life policy (possibly no taxable income ever) to an annuity (possibly lots of taxable income) is "a good thing," and therefore encouraged. Moving in the other direction is not "a good thing" and therefore discouraged. It's also important to note that §1035 has its own definitions of a "life insurance contract", an "endowment contract," and an "annuity contract." Those definitions can be very important in working with clients who have older policies. But that's a topic for another blog.

Section 1035 and the Policy Loan Trap

The rules of §1035 seem reasonably straightforward until you come to the issue of policy loans. If a life insurance policy that has an outstanding policy loan is exchanged for another policy and the loan is not carried over into the new policy the loan is considered "boot" in the course of the transaction and is treated as a LIFO distribution: that is, the disappearing loan will be subject to income taxation to the extent that there is gain in the original policy [IRC §1031(b)]. To illustrate --

Policyholder A exchanges a VUL policy with a basis of $300,000 and $550,000 of Cash Surrender Value for a UL policy, transferring the entire $550,000 as a rollover to the new policy.

Tax result: No tax on the exchange under §1035.

Policyholder B exchanges a VUL policy with a basis of $300,000, a $200,000 loan and $350,000 of net cash surrender value ($550,000 of gross cash value) for a UL policy, transferring only the $350,000 of net cash surrender value as a rollover to the new policy.

Tax result: "Boot" in the course of the exchange to the extent of the gain of $250,000 or the loan, whichever is less. In this case, the entire loan is subject to taxation. $200,000 taxable boot -- $80,000 tax due in a 40% bracket.

You can see the problem this creates: A client exchanges one policy for another, receives no funds in the course of the transaction, and ends up with an unpleasant tax bill at the end of the day. Then they call you.

Loan Rescue to the Rescue

Fortunately, several decades ago the end of tax deductions for personal interest kick-started loan rescue strategies. Since then insurers have been fine-tuning products to make the best out of a bad situation. "Transferring" the policy loan from the old policy to the new policy seemed like a logical solution to the problem of "boot," and has subsequently been blessed by the IRS in Letter Rulings 8806058 and 8604033. Additionally, the IRS reached the same conclusion in Letter Ruling 8816015 where one policy was exchanged for another subject to the same indebtedness and the taxpayer considered making withdrawals or partial surrenders from the new policy to reduce the indebtedness.

Somewhat at odds with these rulings is Letter Ruling 9141025, where a policyholder wanted to exchange a life policy with an outstanding loan but first pay off the loan by withdrawing values and repaying the loan, then exchanging the balance of the policy for a new policy. A seemingly straightforward sequence of events, all contractually allowed and each treated favorably in the tax code. However, in this specific instance the IRS viewed the withdrawal and exchange as a "step transaction." As a result the policyholder was taxed on the withdrawal used to pay off the loan, a withdrawal that would normally be treated as a distribution of non-taxable basis.

Apart from this letter ruling there are a number of policy loan rescue strategies that do not involve withdrawals prior to the exchange and that fall within the purview of the favorable letter rulings cited above (understanding, of course, that the normal caveats about PLRs are always in play).

Design Variables in Rescue Strategies

In the marketplace you have access to products and loan rescue strategies that can work for almost any of your clients. As long as the policy is not too far underwater you can usually find a home for your clients that will improve their cash flow and help preserve their benefits. Variables to be designed around include:

- Loan amount limits – Most companies will place ceilings on the percentage of total value represented by the transferred loan, from 40% up to 90%.

- Loan repayment options – Look for companies that have liberal withdrawal provisions. Companies that are serious about loan rescue will allow withdrawals and loan repayments in the first or second policy year, which helps to get the client out from under the burden of loan interest in a hurry.

- Interest spreads – Interest rate spreads between interest credited and interest accrued on the borrowed funds can make or break a policy's performance. Some products have zero net cost (aka "preferred" and "wash") loans from day one.

- Product types – Not every company makes every product available for loan transfers. Find the best performing products for your client's specific situation.

- Limits based on age, face amount and cash value/loan proportion – Most companies use these restrictions to avoid undesirable results – there are some combinations that just simply won't work.

Other factors to be considered, not specific to loan rescue plans, but often important to the success of the exchange, include.

- Flexible guarantee periods

- Attractive cash value potential based on crediting rates and mortality charges

- Pre-payment discount features

- "Catch-up" features

- Underwriting classes available

- Availability of increasing death benefit options

Any "recipe" for success that combines these features and factors will be specific to your client's circumstances. And because the "ingredients" are constantly changing as products change, your best bet is to call the Windsor design team and ask for their recommendations on the carriers and products that will best suit your client's needs.

Rescue Strategies Come in All Shapes and Sizes

A few of the strategies that come out of these variables include:

Transfer the loan and, if the policy values permit, take withdrawals to repay and eliminate the loan and loan interest.

This is the most common strategy and its effectiveness depends heavily upon the following product provisions:

- Charges for withdrawals – the lower the better

- Restrictions on the timing and number of withdrawals permitted – the fewer the better

- Products available – the more recent the design, the better

- Early year cash values -- the higher the better

Transfer the loan and convert it to a "wash" loan as soon as possible

Another popular strategy, its effectiveness hinges on:

- The amount of loan in proportion to the net cash value – the lower the better

- How much and how quickly the transferred loan and any accrued interest becomes a "wash" loan – the more and the earlier the better

- Current assumption performance – the more competitive the better

- Products available – the more recent the design, the better

Transfer the loan and "crawl out" of the loan by taking incremental withdrawals and making loan repayments over several years until the loan is gone

- Charges for withdrawals – the lower the better

- The amount of loan in proportion to the net cash value – the lower the better

- How much and how quickly the transferred loan and any accrued interest is a "wash" loan – the more and the earlier the better

- Current assumption performance – the more competitive the better

- Products available – the more recent the design, the better

Sidebar: No Gain No Pain

For policies without any gain over investment, there is sometimes no compelling reason to jump through the hoops of Section 1035. A simple combination of applying for and issuing a new policy, and subsequently surrendering an old policy, dispensing with any loans, and using the net cash value as a premium payment, may be a satisfactory, tax-neutral outcome for your client. But even when there's no gain in the old contract you might want to preserve your client's basis for future withdrawals or surrenders. The only way to do that, even with no taxable gain in the contract, is to comply with the rules and procedures of Section 1035.

Tax Reporting Issues

Most life insurance companies agree that the IRS allows loans to be transferred in connection with tax-free policy exchanges. And when they report to the IRS they issue informational (code 6) 1099-R's only. However, handling 1099-R's that report taxable income on the exchange of life insurance contracts is another subject. Some companies routinely report taxable income when there is an outstanding loan on a policy to be exchanged, regardless of the information they receive about the intended transfer of the loan to the new policy. When that happens, here are some alternatives for clients and their advisors to consider:

1) The policy owner can ask the original insurer to issue a corrected form 1099-R and report the policy exchange as tax-free.

2) The policy owner can choose to disclose the exchange on their individual income tax return, but treat the exchange as tax-free. Anyone contemplating this strategy should report the full amount of the gross distribution (the amount shown in box 1 of IRS form 1099-R) on line 16a of the IRS form 1040. Instead of showing the amount in box 2a on the 1099-R form on line 16b of the IRS form 1040, the policy owner would enter a zero on line 16b. Because this will vary from the income reported on the 1099-R form, the policy owner should attach a statement to his or her income tax return explaining that he or she believes the original insurer incorrectly reported the exchange as being taxable.

3) A third alternative is to file an income tax return reporting the full amount of the gain reported by the original company, and paying any required taxes with the tax return. After filing the original return, the individual could request a refund of taxes paid because the exchange should have been treated as being tax-free.

The Good News: You Don't Need to Know All This

It's inevitable. You either have clients now or will have clients soon with policy loan problems. There aren't any quick and easy solutions for every situation, just a maze of possibilities. And loads of opportunities. The best way to find your way through the maze? Get in touch with the case design team at Windsor and let them handle the rest.

Comments